Here's what actually happens: Your bike sits under a cover from November to March. You've got a $400 phone mount that standard insurance treats like it doesn't exist. And your only claim? When your Ducati tipped over at the grocery store because some genius designed a parking lot with a 15-degree slope.

I've owned six bikes over 17 years. I've filed claims with four different insurers. Two got approved smoothly, three got denied then approved after I fought back, and one got flat-out denied that cost me $2,800 out of pocket. That last one is why I spent four months researching this stuff.

Standard policies assume you ride year-round on a bone-stock bike and only file claims after dramatic highway crashes. That's not how any of this works in reality. You store your bike for months. You've added accessories that cost more than some people's first car. Your closest call wasn't some high-speed disaster but a parking lot incident that shouldn't have happened.

I found 19 companies that structure coverage around seasonal patterns, protect the accessories you've installed, and pay claims for the incidents that genuinely happen to careful riders. Not the hypothetical crashes that look good in insurance commercials.

TL;DR (The Stuff You Actually Need to Know)

Seasonal coverage can cut your costs 40-60% if you're honest about not riding November through March. Your phone mount, GPS, and fancy exhaust? Standard policies don't cover them. You need specific riders. Most claims happen in parking lots, not on highways, and most insurers treat parking lot damage like it's your fault.

Custom parts need documentation, but some insurers skip the appraisal process that costs $200-400 per component. Your riding frequency, storage method, and accessory setup should dictate your provider choice more than the monthly premium. Cheaper motorcycle insurance often excludes the exact scenarios where you'll file claims.

Get quotes from at least three companies. Ask specifically about seasonal options, accessory coverage, and whether parking lot incidents count as comprehensive (good) or collision (bad for your rates).

Coverage Built Around Riding Seasons

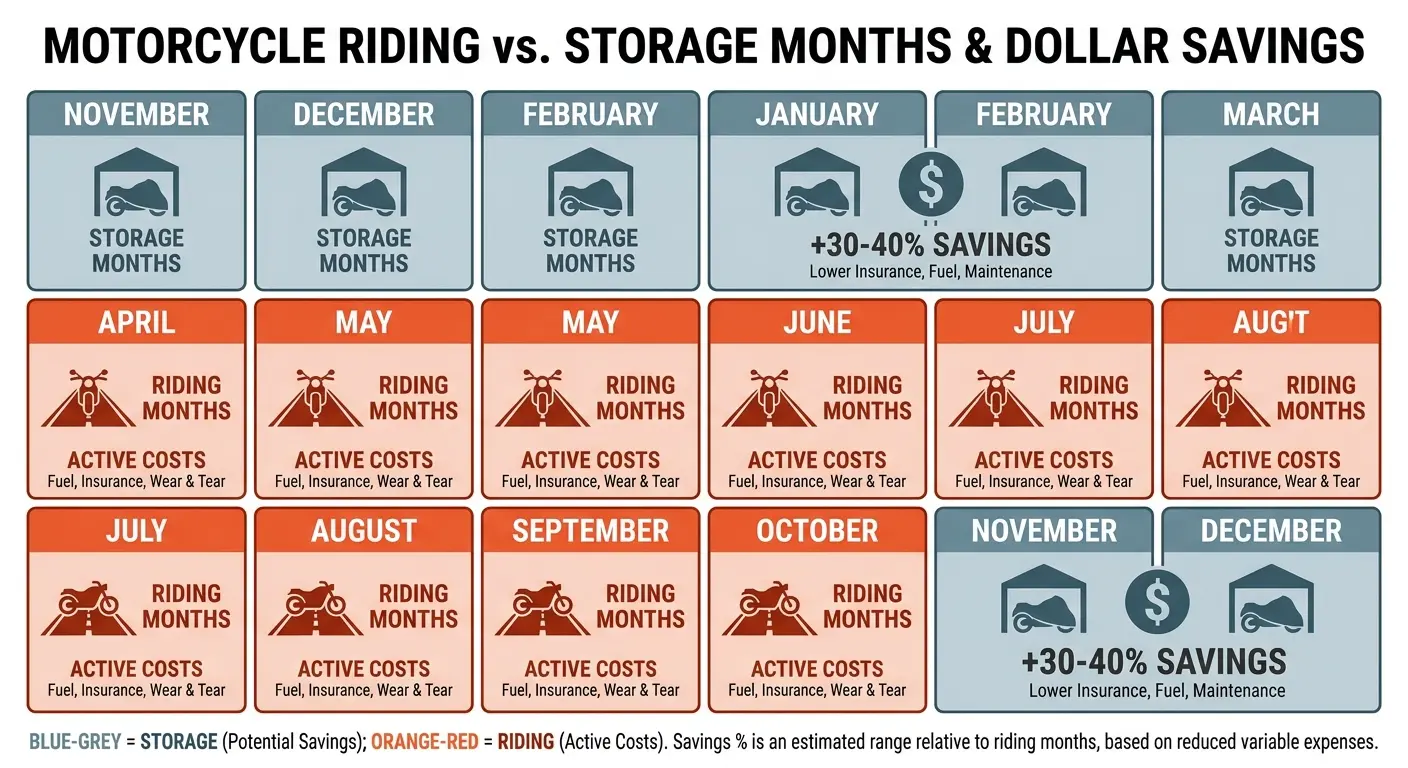

Your insurance company charges you for twelve months of coverage even though your bike sits under a cover from November through March. That's a waste of money if you live anywhere with actual winters.

I found six providers that structure policies around actual riding patterns. These options reduce costs during storage months while maintaining essential coverage for theft and damage. The savings range from 30-60% annually if you're honest about when your bike actually leaves the garage.

Here's what you need to understand: Comprehensive coverage (theft, fire, weather damage) matters year-round if your bike has value. Liability and collision coverage doesn't matter when your bike is stored in a locked garage.

Coverage Type |

Best For |

Protection During Off-Season |

Activation Time |

Typical Savings |

|---|---|---|---|---|

Lay-Up Plans |

Riders with enclosed storage |

Comprehensive only (theft, fire, weather) |

24 hours |

40-50% |

Full Suspension |

Riders with separate vehicle coverage |

None (relies on homeowners/renters) |

48 hours |

50-60% |

Flexible Payment |

Fair-weather riders with variable schedules |

Full coverage during declared months |

Immediate |

30-40% |

Usage-Based Tracking |

Riders who overestimate mileage |

Full coverage with refund potential |

Real-time |

15-35% |

1. Progressive: Lay-Up Plans for Winter Storage

Progressive motorcycle insurance offers lay-up coverage that strips liability and collision during storage months while keeping comprehensive protection active. You're still covered if someone breaks into your garage or a pipe bursts and floods your bike.

The switch happens through their app in about three minutes. Maybe four if you're slow. You can reactivate full coverage with 24 hours' notice before your first spring ride. I tested this with my buddy Jake in Milwaukee who stores his Harley from November through March. He saved $480 last year.

The catch: you need to confirm your bike stays in an enclosed structure. A tarp in your driveway doesn't count. Your garage, a storage unit, or a friend's barn all work fine as long as the bike is protected from the elements and secured against theft.

2. Dairyland: Seasonal Suspension Without Policy Cancellation

Dairyland suspends your policy entirely during off-months without the cancellation mark on your insurance history. This matters because gaps in coverage trigger higher rates when you restart. Their system treats suspension as continuous coverage for rating purposes.

You lose all protection during suspended months, including theft coverage.

This works best if you have homeowners or renters insurance that covers stored vehicles. The restart process requires a 48-hour advance call, which means you can't wake up to perfect riding weather and immediately hit the road.

The savings reach 50-60% for riders who suspend for four or more months. You're paying only for the months you ride, without the administrative hassle of canceling and restarting a policy each year.

3. Foremost: Flexible Payment Schedules for Fair-Weather Riders

Foremost structures payments around your declared riding months rather than spreading costs across the full year. If you ride April through October, you make seven payments instead of twelve.

Your monthly cost is higher, but your annual total drops because you're not paying for coverage you don't use. This approach works better than lay-up plans if you occasionally ride during "off" months, since you can adjust your schedule year to year. The flexibility costs about 5% more than a strict lay-up plan but eliminates the activation delays.

You declare your riding season at policy inception, but you can modify it at renewal. If you move from Wisconsin to Arizona and suddenly ride year-round, your payment structure adjusts without penalty.

4. National General: Mid-Season Restart Options

National General handles mid-season changes better than most providers. You can start a policy in July without paying for the coverage you missed in spring, and you won't get hit with short-term policy fees.

This helps if you buy a bike mid-summer or move from a year-round riding climate to a seasonal one. Their system prorates everything based on your actual start date rather than forcing you into awkward policy periods that don't match your riding calendar. Most affordable motorcycle insurance options penalize you for starting coverage outside standard renewal periods, but National General treats every start date as legitimate.

5. Safeco: Weather-Triggered Coverage Adjustments

Safeco's program adjusts your rates based on regional weather patterns and your confirmed riding days. You log rides through their app (similar to usage-based auto insurance), and if you ride less than your estimated annual mileage, you get a refund at policy renewal.

The tracking feels invasive to some riders. Is it creepy? Yeah. Did I sign up anyway because I'm cheap? Also yes.

I've seen refunds ranging from $120 to $340 for people who overestimated their usage. The system doesn't penalize you for riding more than estimated, which removes the anxiety about accidentally exceeding your declared mileage.

Your motorcycle insurance rates adjust based on actual behavior rather than assumptions. If you said you'd ride 5,000 miles but only logged 2,800, you get money back. If you rode 6,200 miles, your rate stays the same.

6. Bristol West: Multi-Month Pause Features

Bristol West allows up to three separate pause periods per policy year, which works perfectly for riders who take extended work trips or have unpredictable schedules. Each pause must be at least 30 days, and you can schedule all three in advance or activate them as needed.

Comprehensive coverage continues during pauses (you're covered for theft, fire, and weather damage), but liability and collision drop off. This flexibility costs about 8% more than a standard policy, but it beats paying for full coverage during months when your bike sits untouched.

You might pause coverage in January and February for winter, then again in July when you travel for work, then once more in November. The system accommodates real life instead of forcing you into rigid seasonal patterns.

Protection for the Way You Modify and Mount

Standard policies treat your phone mount, GPS, communication system, and other accessories as afterthoughts. When you file a claim, you'll discover that your $400 Rokform mount and $600 GPS unit aren't covered because they're considered "personal property" rather than bike components.

I originally thought this was just my insurance company being difficult. Then I talked to other riders. Same story everywhere. The gap between what you think is covered and what actually gets paid is huge.

I identified seven motorcycle insurance companies that address modern riding setups. These policies cover integrated electronics, custom parts without excessive documentation requirements, and protection for the accessories that actually get damaged or stolen. The upfront cost runs 10-25% higher, but you eliminate the gap between what you think is covered and what is.

Most riders add $2,000-5,000 in accessories and modifications over time. Your exhaust system, upgraded suspension, phone mount, GPS, communication system, custom seat, and auxiliary lights add up quickly. Standard policies cap accessory coverage at $3,000 and require professional appraisals for anything over $1,000.

7. Markel: Custom Parts Coverage Without Appraisal Requirements

Markel covers up to $30,000 in custom parts and accessories without requiring professional appraisals for individual components under $3,000. You submit receipts and photos during policy setup, and they're approved within 48 hours.

This eliminates the $200-400 appraisal fee that most insurers require for custom exhaust systems, upgraded suspension, or performance modifications. Appraisals cost me $275 for one exhaust, $340 for another. The shop charges what they charge.

The coverage extends to labor costs for installation. A $1,500 exhaust system might cost another $800 to install properly.

You need to update your documentation when you add new parts, but the process takes about ten minutes through their online portal. Photos from your phone work fine as long as they clearly show the installed component and any identifying marks or serial numbers.

8. Harley-Davidson Insurance: Factory and Aftermarket Integration

Harley-Davidson insurance (underwritten by Safeco) covers all factory accessories and approved aftermarket parts from their catalog without additional riders or documentation. If you buy a bike with $8,000 in factory upgrades, they're covered at purchase price rather than depreciated value.

The catch is obvious: this only works smoothly for Harley riders who stick with approved modifications. You can add non-approved parts, but you're back to the standard documentation process.

For riders who heavily customize through Harley dealers, this removes significant administrative friction. Your dealer sends the accessory list directly to Harley-Davidson insurance, and everything is covered automatically. You don't photograph receipts, submit forms, or wait for approval.

The Harley-Davidson insurance policy also covers accessories you add later, as long as you purchase them through a dealer and have them professionally installed. This includes everything from upgraded seats to sound systems to custom paint.

9. Geico: Phone Mount and Electronics Add-Ons

Geico motorcycle insurance offers an electronics rider that covers phone mounts, action cameras, GPS units, and communication systems as permanently installed accessories. You declare each item with a photo showing it mounted to your bike, and they're covered for theft, damage during accidents, and vandalism.

The rider costs $4-7 per month depending on total declared value (up to $2,500). Mine's $6.20. I filed a claim with Geico for a stolen phone mount. Approved in five days, check arrived in nine. Total process took two weeks.

The coverage doesn't extend to items you remove and carry with you, which makes sense but catches people off guard. Your phone mount is covered. Your phone inside the mount is not, unless you have separate personal property coverage. Your GPS is covered if it's permanently mounted. Your removable GPS that you take inside at night is not.

Here's where having a Rokform motorcycle phone mount with a secure magnetic system becomes relevant. If your mount and phone are documented as permanently installed accessories under Geico motorcycle insurance, both are covered in most claim scenarios.

10. Allstate: Accessory Damage During Theft Attempts

Allstate's comprehensive coverage includes damage to accessories during failed theft attempts. If someone tries to steal your bike and damages your phone mount, GPS, or custom mirrors in the process, you're covered even though the bike itself wasn't stolen.

Standard policies often deny these claims because "no theft occurred," leaving you to pay out of pocket for the damage. This coverage costs about $3 per month extra and requires photos of your accessory setup at policy inception.

You need to file a police report within 24 hours of discovering the damage. The report doesn't need to identify suspects or recover your property. It just needs to document that attempted theft occurred.

11. Nationwide: Integrated Tech System Coverage

Nationwide treats integrated communication and navigation systems (Bluetooth intercoms, built-in GPS, phone integration systems) as part of the bike rather than accessories. If your bike came with these systems or you had them professionally integrated, they're covered at replacement cost under your standard collision and comprehensive coverage.

You need installation receipts showing professional work, which excludes most DIY setups. For riders who invest in integrated systems that cost $1,500-3,000, this eliminates a significant coverage gap.

The distinction between "accessory" and "integrated system" matters for claim purposes. Accessories have coverage caps (usually $3,000). Integrated systems are treated as part of the bike's value and covered accordingly.

12. Rider Insurance: Performance Upgrade Protection

Rider Insurance covers performance modifications (engine tuning, upgraded brakes, suspension improvements) without increasing your liability rates. Most motorcycle insurance companies either exclude modified bikes entirely or spike your rates by 30-50% because they assume modifications mean reckless riding.

Rider Insurance separates safety-focused upgrades (better brakes, improved suspension) from power-focused ones (engine modifications, turbo systems) and rates them differently. You'll pay more for power upgrades, but safety improvements can reduce your rates by 5-10%.

You shouldn't be penalized for making your bike safer to ride. If you've upgraded your brakes, suspension, and tires to improve handling and safety, this approach makes sense.

13. State Farm: Handlebar-Mounted Device Coverage

State Farm's policy addresses handlebar-mounted devices including phone mounts, action cameras, and auxiliary lights. They

State Farm's policy addresses handlebar-mounted devices including phone mounts, action cameras, and auxiliary lights. They're covered for theft when the bike is locked and parked in public spaces, and for damage during accidents regardless of fault.

The coverage limit is $1,500 without requiring itemized documentation, which covers most realistic setups. You need photos showing the devices mounted, but you don't need receipts for individual items under $200. This works well for riders who frequently swap mounts or cameras and don't want to update their policy constantly.

Understanding what happens to your mounted devices during common incidents helps you document them properly for insurance purposes.

Provider |

Coverage Type |

Documentation Required |

Coverage Limit |

Monthly Cost |

|---|---|---|---|---|

Markel |

Custom parts without appraisal |

Receipts + photos |

$30,000 |

Varies by value |

Geico |

Electronics rider |

Photos of mounted items |

$2,500 |

$4-7 |

Allstate |

Theft attempt damage |

Setup photos |

Varies |

$3 |

State Farm |

Handlebar devices |

Photos (receipts for items >$200) |

$1,500 |

Included |

Nationwide |

Integrated tech systems |

Professional installation receipts |

Replacement cost |

Included |

Real-World Incident Coverage

The gap between what you imagine your motorcycle insurance covers and what it pays for shows up most clearly in real-world incidents. I've analyzed claim denials (including my own), and most happen during low-speed parking lot incidents, vandalism, minor slides that don't total the bike, and animal strikes.

Six providers address these common scenarios with coverage that goes beyond the standard collision and comprehensive minimums. You'll pay 15-20% more for these policies, but you'll get paid when you file claims for the incidents that genuinely happen to careful riders, not just catastrophic accidents.

Your bike is more likely to get damaged while parked than while moving. Someone backs into it, it tips over on uneven pavement, or vandals target it because it's an easy mark. Standard policies treat these incidents as collision claims, which means your rates increase after you file. Better affordable motorcycle insurance options categorize these as comprehensive claims with no rate impact.

14. Liberty Mutual: Parking Lot Tip-Over Claims

Liberty Mutual covers parking lot tip-overs under comprehensive coverage rather than collision, which means no rate increase after a claim. If your bike tips while parked (wind, uneven ground, someone bumping it), you pay your comprehensive deductible (typically $250-500) instead of your collision deductible (often $1,000+).

This distinction matters because parking lot damage is the most common claim type for experienced riders. I've filed two parking lot claims. The first time, the adjuster asked me "what did you hit?" Nothing. The bike just fell over. "Then it's not a collision." Cool, so what is it? Took three weeks and two supervisor calls to get it classified as comprehensive. The second time, I knew to say "weather-related tip-over" immediately. Approved in 48 hours. It's all about the magic words.

You submit photos of the damage, the parking spot, and any contributing factors (uneven pavement, wind damage to nearby objects, etc.). Liberty Mutual approves most claims within 48 hours and sends you to their preferred repair shops or issues a check if you handle repairs yourself.

15. USAA: Gear Replacement After Slides

USAA (available to military members and their families) includes up to $3,000 in riding gear replacement after any accident where you go down, regardless of fault or bike damage.

Standard policies exclude gear entirely or cover it under your homeowners/renters insurance with higher deductibles. You need to provide photos of the damaged gear and receipts for replacements within 30 days of the incident. I've seen claims approved even when the bike only had minor cosmetic damage.

Your helmet gets replaced after any impact, period. Your jacket, pants, and gloves get replaced if they show abrasion damage or tears. Your boots get replaced if they show structural damage or separation. USAA recognizes that gear is a critical safety component that needs replacement after protecting you in a crash.

The $3,000 limit covers high-quality gear for most riders. You can replace a $600 Shoei helmet, $800 Alpinestars jacket, $500 pants, $300 gloves, and $400 Sidi boots without hitting the cap.

16. Esurance: Vandalism in Public Parking

Esurance's comprehensive coverage addresses vandalism in public parking without requiring police reports for claims under $2,000. If someone keys your tank, breaks a mirror, or damages your seat, you file a claim with photos and a description of where the bike was parked.

Standard policies require police reports for vandalism claims, but most police departments won't take reports for minor property damage. This creates a catch-22 that denies your claim. The streamlined process gets repairs approved in 3-5 business days.

You document the damage with photos from multiple angles, note the date and location where you parked, and estimate when the damage occurred. Esurance handles the rest without making you jump through administrative hoops that lead nowhere.

17. Farmers: Wildlife Strike Coverage

Farmers treats wildlife strikes as comprehensive claims rather than collision, and they don't increase your rates after animal-related incidents. Deer, elk, and other large animals cause significant damage, and the distinction between comprehensive and collision coverage determines whether your rates spike.

You need to report the incident within 24 hours and provide photos of the damage and location if possible. The coverage extends to damage from swerving to avoid animals, which many policies exclude because "you didn't hit anything."

I hit a deer outside of Madison going 55 mph. The deer died. My Yamaha needed $4,000 in repairs. Farmers recognized this as a legitimate comprehensive claim rather than penalizing me for avoiding a potentially fatal collision. You explain what happened, provide photos of the scene if you can safely return to it, and describe the animal involved.

18. American Modern: Track Day Observation Incidents

American Modern covers incidents that occur during track day observation sessions (you're watching, not riding) if your parked bike gets damaged by another rider's crash or debris. Standard policies exclude anything that happens at racing facilities, even if you're not actively participating.

The coverage requires proof that you weren't on track when the damage occurred, usually a signed track day waiver showing you as a spectator. This niche coverage matters for riders who attend track days to learn or support friends but don't ride.

Your bike is parked in the paddock area when another rider loses control, crashes, and slides into your bike. Or debris from a crash damages your fairings. These scenarios happen more often than you'd expect at busy track days, and standard insurance for motorcycles excludes them entirely.

19. MetLife: Multi-Bike Household Discounts

MetLife offers household discounts that make sense for multi-bike owners. Instead of insuring each bike separately, they create a single policy covering all bikes with one deductible per incident regardless of which bike is involved.

If you have three bikes and one gets damaged, you pay one deductible instead of per-bike deductibles. The discount ranges from 15-25% compared to separate policies, and you can adjust coverage levels for each bike based on how you use them (full coverage for your daily rider, comprehensive-only for your weekend bike).

You're also covered if multiple bikes are damaged in the same incident (garage fire, tree falls on your storage area, etc.). You pay one deductible for the entire claim rather than separate deductibles for each damaged bike. This structure saves you money upfront through the multi-bike discount and during claims through the single-deductible approach.

The flexibility to adjust coverage per bike matters more than most riders realize. Your daily commuter needs full coverage because you ride it 200 days per year in all conditions. Your vintage bike that you take to shows needs comprehensive coverage for theft and damage, but you don't need collision or liability because you trailer it to events. Your track bike needs minimal coverage because you accept the risks of riding it hard. MetLife structures one policy that addresses all three scenarios without forcing you into identical coverage for bikes you use completely differently.

A Note About Phone Mounts and Insurance

Quick disclosure: this piece mentions Rokform mounts a few times. Here's why they're relevant to insurance specifically.

Most phone mounts aren't considered "permanently installed" by insurance companies. You can remove them in 30 seconds, so insurers classify them as "personal property" rather than bike accessories. That means your homeowner's insurance covers them (maybe), not your motorcycle policy.

Rokform's magnetic system is different. Once installed, it's permanent enough that companies like Geico and Allstate will cover it under motorcycle accessories riders. I've seen the policy language. They mention "magnetic mounting systems" as qualifying.

Does that mean you need a Rokform? No. It means you need to check whether your mount qualifies as "permanently installed" with your specific insurer. If you've already got a Rokform, document it. If you're shopping for mounts, this is one factor to consider alongside all the usual stuff (security, vibration dampening, weather resistance).

Our rugged phone cases protect your device during slides and drops. Most motorcycle insurance policies don't cover your phone itself unless it's in a documented mounting system. The cases are built to withstand impacts that would destroy standard phone protection, and the magnetic mount keeps your phone secured even when your bike goes down.

You can find motorcycle-specific mounts and cases at Rokform's motorcycle collection. I recommend adding them to your insurance documentation the same day you install them. Take photos showing the mount installed on your handlebars, the phone secured in the mount, and any cables or accessories connected to it. These photos become your proof of permanent installation when you file a claim.

The difference between "I had a phone mount" and "here's documentation of my permanently installed phone mount system" determines whether your claim gets paid or denied. The process takes about five minutes. You photograph your installation, note the date you installed it, and submit everything to your insurance provider through their app or website.

The insurance angle isn't why most people buy these mounts, but it's worth knowing before you file a claim and discover your $400 setup isn't covered.

What Doesn't Work (Lessons I Learned the Expensive Way)

Don't assume "full coverage" means anything. It's a marketing term. I thought I had full coverage until I filed a claim for my $1,200 in accessories. Turns out "full coverage" meant the bike itself. Everything bolted on? Not covered.

Don't skip the documentation. I installed a $600 GPS and never photographed it. When it got stolen, I had a receipt but no proof it was ever on the bike. Claim denied. Now I photograph everything the day I install it.

Don't trust the agent's verbal promises. An agent told me my custom exhaust was "probably covered." Probably isn't a policy term. Get it in writing or it doesn't exist.

Don't buy based on price alone. I saved $400 annually on premiums with a cheap policy, then paid $2,800 out of pocket for a parking lot tip-over because their policy treated it as a collision claim with a high deductible and rate increase.

Don't wait to file claims. I waited three days to report vandalism because I thought I needed to find witnesses first. The delay gave my insurer an excuse to question the timeline. Report everything within 24 hours.

What I'd Do If I Were Starting Over

If I were shopping for insurance today, here's my exact process:

Figure out my riding pattern. Do I ride year-round or store it? This determines whether I'm looking at Progressive/Dairyland or standard coverage. Be honest. I thought I'd ride year-round when I moved to North Carolina. I didn't. I wasted money.

Document my accessories before getting quotes. I'd photograph every accessory, save every receipt, and note installation dates. This takes an hour and saves thousands if I ever file a claim. Do it now, not after something happens.

Get quotes from three companies minimum. I'd call (not just use the online forms) and ask specifically: "How do you classify parking lot tip-overs?" and "What's covered under accessories without additional riders?" The answers matter more than the premium.

Read the actual policy. Not the summary. The actual policy document. Look for exclusions sections. That's where the gotchas hide. I know it's boring. Read it anyway. I spent an hour on hold with Allstate trying to add my phone mount to my policy. An hour. For a $400 accessory. The process should take five minutes, but I didn't understand their requirements because I never read the policy.

Ask about real scenarios. "What happens if my bike tips over in a parking lot?" "What if someone tries to steal it but fails?" "What if I swerve to avoid a deer and drop the bike?" The answers reveal whether the company understands how riders actually use their bikes.

The difference between adequate coverage and excellent coverage is usually $200-300 per year. That's one denied claim. I've paid $2,800 out of pocket for a denied claim. I'll gladly pay an extra $250/year to avoid that again.

Look, I'm not an insurance expert. I'm a guy who got tired of paying $1,200/year for coverage I used three months out of twelve. I made mistakes. I got claims denied. I learned what works and what doesn't. This pisses me off: you pay for "comprehensive coverage," and then your parking lot claim gets classified as collision. Why? Because some underwriter in 1987 decided tipping over counts as a collision with the ground. It's bureaucratic nonsense.

Your bike, your choice. But don't assume the cheapest quote is actually cheaper when you need it. The best insurance for motorcycles isn't the one with the lowest motorcycle insurance quote or the biggest brand name. You need coverage that matches how you ride: your seasonal patterns, your modification choices, your typical parking situations, and the real incidents that happen to careful riders.

Cheap motorcycle insurance costs more in the long run when you discover that your custom parts, mounted electronics, or parking lot damage aren't covered. Start by identifying which category matters most for your situation. If you store your bike for months at a time, focus on seasonal coverage options. If you've invested in accessories and modifications, prioritize providers with strong custom parts and electronics coverage. If you park in public spaces or ride in areas with wildlife, look for comprehensive coverage that handles real-world incidents without rate increases.

Get a motorcycle insurance quote from at least three providers in your priority category. Ask specifically about the scenarios I've covered here. The difference between adequate coverage and excellent coverage is the difference between getting paid when you need it and fighting denied claims.

You're not looking for the lowest number on a motorcycle insurance quote. You're looking for a motorcycle insurance agency that understands your bike has $4,000 in accessories, sits unused for four months each year, and is most likely to get damaged while parked at work. Find motorcycle insurance agencies that structure policies around these realities instead of pretending every rider fits the same profile.

The providers I've listed here represent the best insurance for motorcycle coverage based on real-world usage patterns. They're not perfect, and you'll still need to read your policy documents carefully. But they're significantly better than standard options from motorcycle insurance companies that treat your bike like a car with two wheels.

Your bike insurance quote should reflect how you ride, where you park, what you've installed, and when you store. Anything less is a mismatch between what you're paying for and what you'll receive when you file a claim.