Americans spent $8.3 billion on cracked phone screens in 2023. That's billion with a B. Triple what we spent in 2018. And you know what the phone insurance industry did in response? They refined their claim forms. They adjusted their premiums upward. They did everything except address why so many phones are getting destroyed in the first place.

There's a reason for that. Prevention doesn't create recurring revenue. Monthly premiums do.

Look, I'm not saying these plans are useless for everyone. If you drop your phone twice a month, maybe you need one. But for most people? It's a bad deal. And I'm going to show you exactly why.

Table of Contents

The Insurance Industry's Favorite Blind Spot

You're Subsidizing Someone Else's Cracked Screen

Those "Affordable" Deductibles Aren't So Affordable

Claim Denials Nobody Warns You About

The Fake Choice Between Cases and Coverage

Your Replacement Phone Might Be a Dud

How They Profit From Your Panic

The Math They Don't Want You to See

When Your Plan Expires But Your Phone Doesn't

What You Should Actually Do

TL;DR

Phone insurance costs more than prevention. The math doesn't work for most people. A good case costs $80 once. Insurance costs $360 over two years, plus deductibles. Read on to find out exactly how much you're probably wasting.

The Insurance Industry's Favorite Blind Spot

Protection plans make money when you pay premiums and don't file claims. That's not cynicism, it's basic insurance economics.

While the frequency of smartphone damage saw a slight decrease (78 million Americans reported damaged devices in the past 12 months compared to 87 million during a comparable period in 2020), the business model hasn't changed, according to Allstate Protection Plans' Mobile Mythconceptions Survey. The industry still profits most when customers pay premiums without filing claims.

Every month you send $12 or $15 to a carrier or third-party insurer, you're contributing to a pool that covers the minority of customers who experience device damage or loss. The system works (for the provider) because most people overestimate their risk. You remember that one time you dropped your phone in a parking lot, so you're convinced it'll happen again. The insurance company knows statistically it probably won't, at least not often enough to exceed what you'll pay in premiums.

The Reactive Revenue Model

And here's the thing they really don't want you to know.

The industry has zero financial incentive to help you avoid filing a claim through prevention. They're not sending you high-quality protective gear with your monthly payment. They're not educating you on the most common damage scenarios and how to avoid them. They're simply waiting for you to either break your phone (and pay a deductible) or not break it (and keep paying premiums).

My coworker Sarah paid $15 a month for 18 months. That's $270. She never filed a claim, not once. Her phone has a tiny scratch from being in her purse with her keys, but it still works fine. When I asked her why she kept paying, she said "Just in case." Just in case what? In case she needs to pay another $149 deductible on top of the $270 she already spent?

The math doesn't math.

Meanwhile, her neighbor Jake filed two claims in the same period. Sarah's premiums helped fund Jake's repairs, while she received nothing in return for her careful phone handling.

Why Prevention Doesn't Scale (For Them)

If a protection plan provider sold you a $60 case that prevented the damage their insurance covers, you'd stop needing the insurance. That's a one-time transaction replacing a 24-month revenue stream.

The business model collapses.

This is exactly why carriers push phone protection plans at the point of sale but treat physical protection as an afterthought. You'll get a hard sell on the monthly plan, maybe a half-hearted gesture toward a basic case sitting in a sad little display rack nobody looks at, and that's it.

The economic incentives point toward recurring payments, not problem-solving.

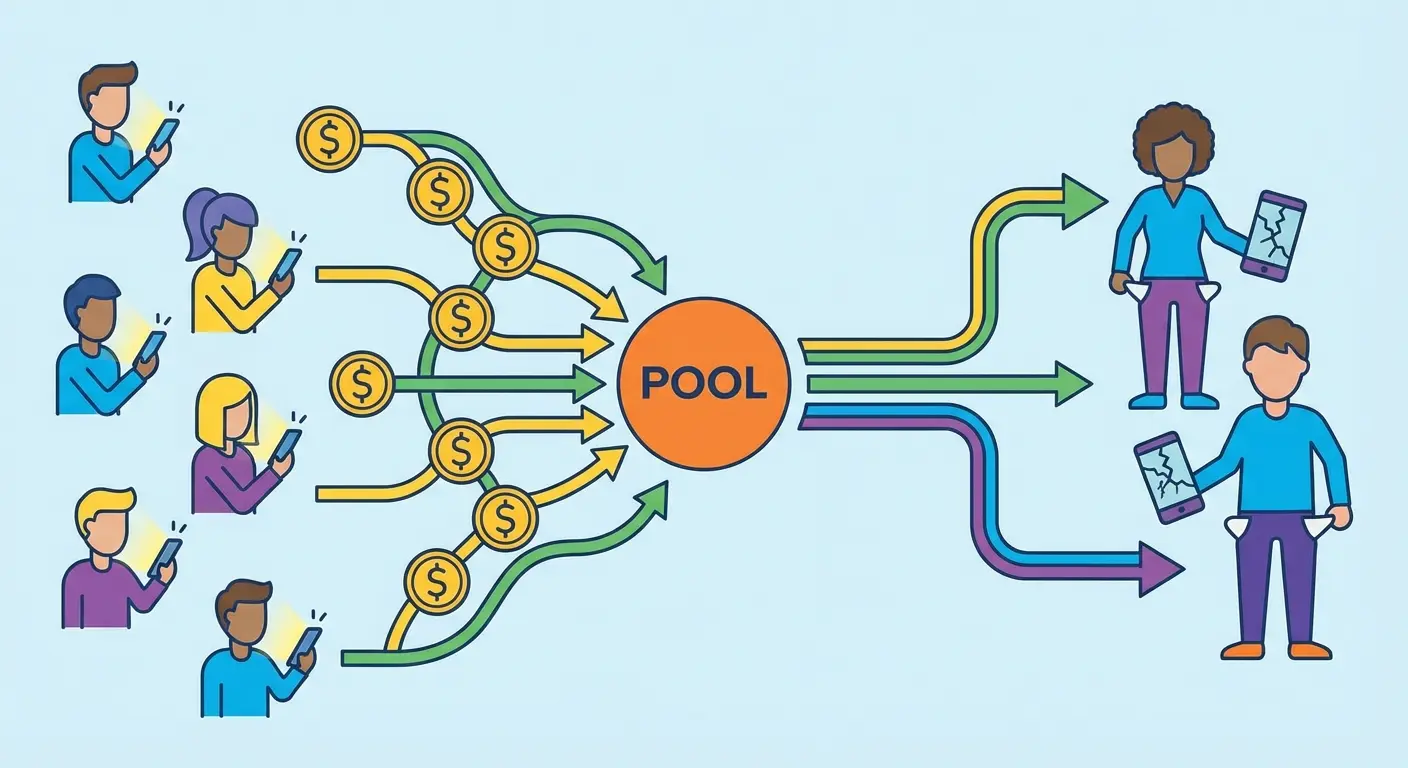

You're Subsidizing Someone Else's Cracked Screen

Most people don't realize they're subsidizing repairs for the small percentage of users who file multiple claims. The math of protection plan pooling reveals exactly how your money flows through the system, and who benefits most.

Protection plans operate on risk pooling. Your $15 monthly payment joins thousands of others in a fund that covers claims. Sounds reasonable until you realize you're paying the same rate as someone who's filed three claims in six months.

There's no good behavior discount. No reward for keeping your device intact.

You and the person who drops their phone monthly pay identical premiums. The careful user subsidizes the careless one, and the system is designed exactly that way. Carriers know that roughly 20-30% of plan holders will file a claim during the coverage period. They price premiums to cover those claims, administrative costs, and profit margins.

Everyone pays for the minority's damage.

User Profile |

Premium Paid (24 months) |

Claims Filed |

Net Cost to User |

Subsidy Direction |

|---|---|---|---|---|

Careful User (no claims) |

$360 |

0 |

$360 |

Subsidizes others |

Average User (1 claim) |

$360 |

1 ($149 deductible) |

$509 |

Roughly break-even |

Frequent Claimant (3 claims) |

$360 |

3 ($447 in deductibles) |

$807 |

Subsidized by others |

Actual Repair Cost |

N/A |

N/A |

Varies $150-600 |

Provider's actual expense |

The Psychological Pricing Sweet Spot

Fifteen dollars a month doesn't trigger our mental alarm bells. It's less than a couple of coffee runs, barely noticeable on a monthly phone bill that's already $80 or more.

That's intentional.

Break that down annually ($180) or over a typical two-year device cycle ($360), and the math starts looking different. You're paying enough to cover a quality protective case, a screen protector, and still have money left over. But spreading it across 24 months keeps it under the threshold where most people would question the expense.

Those "Affordable" Deductibles Aren't So Affordable

Deductibles represent the second payment in a two-payment system, but most people don't factor them into their cost analysis when signing up. These charges have climbed steadily over the past five years, now ranging from $99 for screen repairs to $249 for full device replacements with premium phones.

You've paid $15/month for eight months ($120) when you finally drop your phone hard enough to crack the screen. You file a claim, feeling relieved you have coverage.

Then comes the deductible: $149 for screen damage on a premium device.

Your total cost for that single repair? $269. Many third-party repair shops would've fixed that screen for $150-200. You've paid extra for the privilege of paying more.

The Second Bill You Forgot About

Device replacement deductibles hit even harder. That $249 deductible plus six months of premiums ($90) means you're $339 deep before you get a replacement phone. And that replacement? It's probably refurbished. We'll get to that.

Michael cracked his iPhone 15 Pro screen when it slid off his dashboard during a sudden stop. He'd been paying $17/month for almost a year, so $170 total. The deductible? $149. He's $319 deep. Later he found out the Apple Store would've done it for $279. A local repair shop quoted $220.

He paid extra for the "convenience" of using insurance that cost him an extra $40-100.

He was not happy when I showed him the math.

Deductibles Keep Climbing

Five years ago, typical deductibles hovered around $50-75 for screen repairs. They've nearly doubled while monthly premiums have also increased. Providers justify this by pointing to rising device costs, but repair costs haven't increased at the same rate.

You're paying more monthly AND more per claim, while the service (repair or replacement) costs the provider roughly the same. The margin expansion is significant, and it's coming directly from your pocket.

Claim Denials Nobody Warns You About

You don't read the full terms and conditions when you're signing up for a protection plan at the carrier store. You're excited about your new phone, the salesperson is moving quickly, and the plan sounds straightforward: pay monthly, get coverage, file claims if needed.

The exclusions and limitations reveal themselves later, usually right when you need the coverage most.

That crack on the back of your phone? They're calling it "pre-existing damage" even though it happened yesterday. You dropped it in a puddle? That might be classified as "water damage due to misuse" rather than accidental damage.

When "Covered" Doesn't Mean Covered

Denial reasons often hinge on interpretation. What counts as "normal wear and tear" versus "accidental damage"? Who decides if damage was pre-existing?

The provider does, and they're financially motivated to classify claims in ways that limit payouts.

Some plans require you to file within 60 days of purchase for certain types of damage, a window that's easy to miss if you don't discover the damage immediately. Others require a police report for theft claims filed more than 24 hours after the incident. These aren't unreasonable requirements in isolation, but they create barriers that reduce claim approval rates.

And good luck appealing. They've made that process just painful enough that most people give up and pay for repairs themselves.

The appeals process exists, but it's deliberately cumbersome. You'll spend time on hold, submit additional documentation, and possibly escalate through multiple levels. Most people give up and pay for repairs themselves, which is exactly what they're counting on.

If you're going to get one of these plans anyway, here's what you need to know: Document your phone's condition with photos immediately after purchase and periodically thereafter. That "pre-existing damage" claim is harder to make when you've got timestamped photos. Note your plan's claim filing window (typically 60-90 days for certain damage types) and set calendar reminders. For theft, file a police report within 24 hours. For damage, take clear photos showing the extent and nature of the incident.

And never, ever attempt repairs or take your device to non-approved repair shops before filing a claim. That voids coverage faster than anything.

The Fake Choice Between Cases and Coverage

You can buy a protection plan. You can buy a protective case. But you'll rarely find a provider offering both as an integrated solution at a reduced combined price.

That's not an oversight.

Bundling physical and financial protection would reduce claims (good for you, bad for their revenue model) and create price transparency that makes the monthly premium harder to justify. If a carrier said "Here's a $70 case and a $10/month plan with a reduced deductible because you're using quality protection," you'd immediately start doing math on whether the plan is necessary.

Coverage vs. Prevention

Financial protection feels like it covers everything because it addresses multiple scenarios: drops, spills, theft, loss, mechanical failure. Physical protection feels limited because it only prevents some types of damage.

This perception ignores effectiveness rates.

A quality protective case prevents the vast majority of drop damage, which represents the most common claim type. Screen protectors prevent or minimize screen damage, the second most common claim. Secure mounting systems prevent drops in vehicles, another frequent damage scenario.

Financial protection covers more scenarios but prevents none of them. Physical protection covers fewer scenarios but prevents most of them.

Yet we're conditioned to value the former over the latter.

Get this: According to Allstate Protection Plans' research, damaged screens account for 67% of smartphone accidents and malfunctions. That's two-thirds of all problems. Physical protection directly addresses the single largest damage category, yet it's treated as secondary to insurance plans.

Your Replacement Phone Might Be a Dud

When you file a device replacement claim, you're almost never getting a new phone. Understanding what "certified refurbished" means, how refurbishment standards vary between providers, and why your replacement might have a shorter lifespan than your original device matters more than marketing materials suggest.

Your $900 phone gets stolen. You file a claim, pay your $249 deductible, and wait for the replacement. What arrives is a "certified refurbished" device that may have been through one or more previous owners.

Refurbishment standards vary wildly. Some providers do thorough testing and part replacement. Others do minimal inspection and cleaning. You won't know which you're getting until it arrives.

The Battery Life Lottery

Refurbished phones often have batteries with degraded capacity. Your replacement might arrive with 85% battery health, meaning it won't hold a charge as long as your original device did when new. Most protection plans don't guarantee battery condition in replacements.

You might get lucky with a recently refurbished device that has a new battery. You might get unlucky with one that's been through multiple charge cycles and shows its age. There's no way to know beforehand, and by the time you discover the battery life is terrible, you've already paid the deductible and your claim is closed.

When you eventually upgrade and want to sell or trade in your phone, its history matters. A device that's been through a refurbishment process and insurance replacement may have a different IMEI or serial number flagged in databases. Some trade-in programs offer lower values for devices with replacement history.

Your protection plan solved one problem but created another that won't surface until months or years later.

How They Profit From Your Panic

You're at the carrier store, excited about your new phone. The salesperson transitions smoothly from device features to protection: "You'll want to protect this investment, right? These phones are expensive to repair."

They might show you photos of shattered screens or tell you how much an out-of-warranty repair costs. The implication is clear: you'd be foolish not to protect a $1,000 device with a $15/month plan.

What they won't show you: the probability you'll need to file a claim, the total cost you'll pay over two years, or the deductible you'll owe if you do file.

Those details don't create urgency.

The Commission Structure

Sales representatives often earn commission or meet quotas based on protection plan enrollment. The rep isn't trying to scam you. They're working within a system that rewards plan sales and makes it easy to position protection as a no-brainer.

You're making a decision in an environment designed to guide you toward one specific outcome.

Phone protection plans have become so standard that not buying one feels risky. We've shifted from "should I get insurance for my phone?" to "which insurance should I get?"

Once the question is which plan rather than whether you need a plan, they've already won. You're comparing features and prices within their ecosystem rather than questioning the ecosystem itself.

The Math They Don't Want You to See

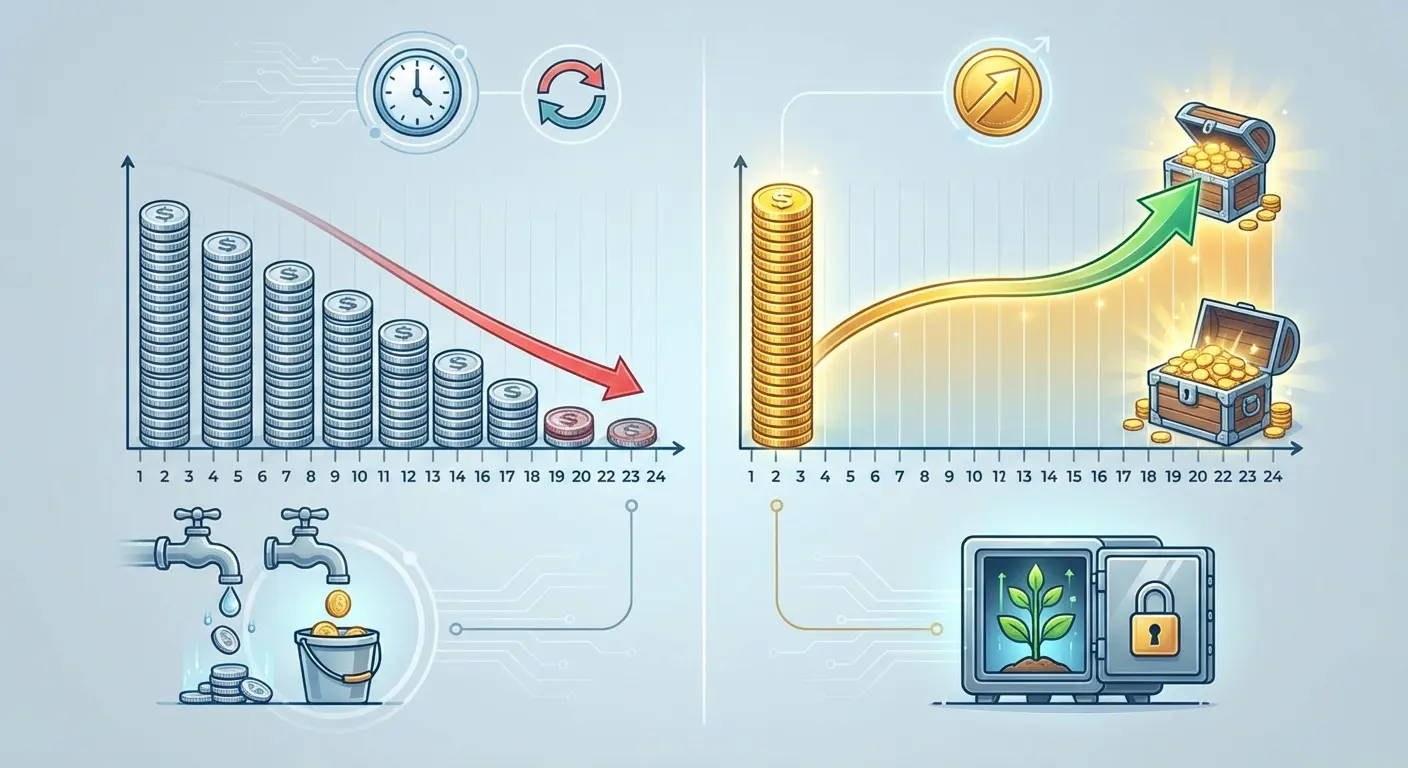

Running the numbers comparing protection plan costs over a typical device ownership period against the cost of quality physical protection and occasional out-of-pocket repairs reveals something interesting. For most users (those who aren't chronically accident-prone), investing in prevention and self-insuring for catastrophic loss costs less and provides better protection.

Protection plan: $15/month x 24 months = $360

Quality protective case: $60-80

Premium screen protector: $30-40

Total prevention cost: $90-120

You're $240-270 ahead with the prevention approach before any damage even occurs.

Now add in the scenario where damage does happen.

When Something Actually Breaks

You drop your phone and crack the screen.

Protection plan route:

Premiums paid (12 months): $180

Deductible: $149

Total cost: $329

Prevention plus out-of-pocket repair route:

Case and screen protector: $100

Third-party screen repair: $180

Total cost: $280

You're still ahead by nearly $50, and your phone wasn't in a protection plan's refurbished replacement pool. You got your actual device repaired and back.

The No-Incident Scenario (Which Is Most People)

You make it through two years without significant damage because you invested in quality physical protection.

Protection plan route:

Total paid: $360

Benefit received: Peace of mind (no service used)

Prevention route:

Total paid: $100

Benefit received: Peace of mind AND damage prevention AND you still have $260

The case and screen protector don't disappear when you don't use them. They're actively working every single day, preventing the drops and impacts that would've led to damage. The protection plan only activates after damage occurs.

Lisa bought a Samsung Galaxy S24 Ultra and immediately invested $85 in a military-grade case and tempered glass screen protector. Over the next two years, she dropped that phone four times. Once on concrete, twice on tile floors, and once down a full flight of stairs (which honestly should've killed it). Each time, the case did its job. Her total protection cost: $85.

Her coworker David has the same phone. He went with the carrier's $17/month plan and a cheap $15 case. Two years later, he's paid $408 in premiums. He never filed a claim because nothing bad enough happened to justify the $149 deductible.

Lisa spent $323 less. And honestly? She probably had better actual protection.

What You're Really Giving Up

That $360 over two years could fund your next phone upgrade, cover accessories you actually want, or simply stay in your account. We don't think about protection plan costs this way because they're hidden in monthly increments, but the opportunity cost is real.

Every dollar going to premiums is a dollar not available for something else. The question isn't whether you can afford $15/month (most people can), it's whether that's the smartest use of those dollars given your actual risk.

When Your Plan Expires But Your Phone Doesn't

Most people keep their phones longer than protection plans remain economically viable. In year three and beyond, monthly premiums often increase, deductibles stay high or rise, and the replacement value of your device has depreciated significantly.

Consumer advocacy groups are increasingly calling this out. Kevin Brasler, executive editor at Consumers' Checkbook, straight-up told WCVB in October 2025 that phone protection plans "are really bad deals for consumers" and noted they're "enormously profitable for the companies that sell them and for the insurance companies that back them, but they are way overpriced for the coverage that they provide." When the consumer protection people are saying it's a ripoff, maybe listen?

His organization recommends canceling phone protection plans after two years maximum, or three years at the absolute most.

The Third-Year Trap

You've kept your phone for three years because it still works fine. Your protection plan premium is still $15/month (or has increased to $17 or $18). Your deductible is still $249. But your phone's replacement value has dropped to maybe $300-400.

The math stops making sense.

You're paying $180+ annually to insure a device worth $350, with a deductible that's 70% of its value. Yet canceling feels risky after investing $540 over the previous two years. That's called the sunk cost fallacy, and they're counting on it.

Some plans increase premiums for older devices or limit coverage after a certain period. You might find that theft coverage drops off after 24 months, or that mechanical failure claims aren't accepted on devices over three years old. The fine print you didn't read at signup becomes relevant exactly when you need it.

Phone protection plans create subtle pressure to upgrade on the carrier's preferred schedule. When your plan becomes cost-prohibitive for an older device, upgrading to a new phone and new plan starts looking reasonable.

That's not accidental.

When to Cancel Your Protection Plan:

Your phone is fully paid off and no longer financed. The annual premium cost exceeds 25% of your phone's current resale value. You've had the phone for 24+ months and haven't filed any claims. Your deductible is more than 60% of your device's replacement value. You would choose to upgrade rather than repair if something happened. You've invested in quality physical protection that's working well. Your credit card offers phone protection that covers your needs.

What You Should Actually Do

Alright, let's put this all together. A hybrid approach combines high-quality physical protection with strategic, minimal insurance coverage for specific scenarios (primarily theft and loss, which physical protection can't prevent).

The movement toward smarter phone protection extends beyond individual consumer choices. Public Interest Research Groups (PIRG) published guidance in 2025 recommending that consumers skip traditional phone protection plans entirely, noting that "phone protection plans are profitable for companies precisely because most customers pay more in premiums than they ever claim in benefits." PIRG suggests creating a dedicated "phone emergency fund" by depositing the monthly premium amount into savings instead, giving consumers control over their protection dollars while building a repair fund that stays with them if never needed.

Start With Prevention, Add Coverage Strategically

Your first dollar should go toward physical protection that prevents damage. A quality case that can handle drops from six feet, a screen protector that absorbs impact, and secure mounting systems for your car create a foundation that insurance plans can't match.

Once you've invested in prevention (that $90-120 range we discussed), evaluate what risks remain. Physical protection won't help if your phone gets stolen or you leave it in a rideshare. Those scenarios might justify minimal insurance coverage.

Be Honest About Your Actual Risk

Do you drop your phone monthly or have you gone years without an incident? Do you frequently travel to high-theft areas or mostly stay in low-risk environments? Do you have a history of losing items or are you generally careful with your belongings?

Your answers should drive your coverage decisions.

Someone who's never filed a claim and uses quality protection probably doesn't need a comprehensive plan. Someone who's filed three claims in two years might benefit from coverage despite the cost, though honestly they should probably just invest in better physical protection.

Check What You Already Have

Look at your credit card benefits before buying a carrier plan. Many premium credit cards include phone protection (typically $600-800 coverage with a $25-100 deductible) if you pay your monthly phone bill with that card.

Manufacturer programs (like AppleCare+) often provide better coverage than carrier plans, with lower deductibles and guaranteed new or like-new replacements rather than refurbished devices. They cost more upfront but the total cost over two years is often comparable with better terms.

When Plans Actually Make Sense

Phone protection plans aren't universally bad. They make sense for specific situations:

You have a documented history of frequent damage (multiple incidents per year). You work in environments with high damage risk (construction, outdoor work, etc.). You live in or frequently visit high-theft areas and worry about device security. You have young children who regularly use your device. You simply can't afford a $300-500 emergency expense if something catastrophic happens.

If any of these apply, a protection plan might be worth the cost. Just go in with eyes open about the total expense, deductible structure, and refurbishment policies.

The Sweet Spot

For many people, the answer is quality physical protection plus minimal catastrophic coverage. Invest in a case and screen protector that prevent damage. Add theft and loss coverage only (many carriers offer this as a cheaper tier) if you're concerned about those specific scenarios.

You're protecting against the most common damage types through prevention while maintaining a financial safety net for the scenarios prevention can't address. Total cost is lower than comprehensive insurance, and you get better protection where it matters most.

Prevention That Works (And Why We Built What We Built)

Alright, full disclosure time. I work for Rokform, and yeah, we make phone cases. But hear me out on why that matters for this conversation.

You've been paying monthly premiums for coverage that only activates after your phone is already damaged. That's backwards.

We built Rokform because we kept seeing the same scenario: people dropping phones during activities, in vehicles, or just during daily life because their cases couldn't handle real-world impacts or didn't provide secure mounting options. Standard cases might protect against minor bumps, but they fail during the drops that matter.

Our cases use a polycarbonate and TPU combination that's been drop-tested to military standards (MIL-STD-810G). That's not marketing speak. It's tough as hell. We've dropped phones from six feet onto concrete repeatedly and the phone inside survived intact. The raised edges protect your screen and camera even when the phone lands face-down.

Protection during drops is only part of the equation. Most phone damage happens because devices aren't secured properly. They slide off dashboards during turns, fall out of pockets during activities, or get knocked off surfaces.

Our integrated magnetic mounting system (RokLock) creates a secure connection that holds your phone in place whether you're mountain biking, driving, or just need hands-free access. The magnets are strong enough to hold your phone securely through impacts and movement, but they won't mess with your device's functionality or wireless charging.

This is prevention that works. Not insurance that pays out after damage occurs, but physical protection that stops the damage from happening in the first place. You're spending once (not monthly) on a solution that actively protects your device every single day.

What makes Rokform the top choice for serious phone protection? We've engineered every detail around real-world use. Our cases don't just meet military drop standards, they exceed them in testing. The dual-layer construction absorbs and disperses impact energy across the entire case structure, not just at the point of contact. Our magnetic system isn't an afterthought stuck onto a standard case. It's integrated into the case architecture for strength and reliability.

We've tested our cases in conditions that would destroy standard protection: repeated six-foot drops onto concrete, extreme temperature fluctuations, moisture exposure, and sustained vibration. They keep working. The RokLock magnetic system has been tested to hold phones securely at forces exceeding what you'd experience in any normal activity, from aggressive mountain biking to off-road driving.

Is it the cheapest case out there? No. But neither is paying $15 a month for two years.

Check out our full case lineup and find the protection that fits your device and lifestyle. Your phone (and your wallet) will thank you.

Final Thoughts

Look, nobody's going to stop you from buying phone insurance. Maybe you need it. Maybe you're clumsy as hell and drop your phone twice a week. Fine.

But most of you don't. Most of you are paying $15-20 every month for coverage you'll never use, with deductibles that cost almost as much as just paying for repairs yourself, for replacement phones that might have degraded batteries.

That's not protection. That's a subscription service for peace of mind that you could get cheaper and better with an $80 case.

The protection plan industry has convinced millions of people to pay monthly for coverage they'll probably never use, with deductibles that approach the cost of out-of-pocket repairs, for replacements that might be refurbished devices with questionable battery life. That's not a conspiracy, it's a business model. And it's a business model that works better for providers than for most users.

You don't have to participate in a system designed around reactive coverage when proactive prevention costs less and works better. Quality physical protection prevents the vast majority of damage scenarios that insurance covers. The difference is that prevention works every day, not just after something goes wrong.

Do the math. Be honest about how often you actually break your phones. And stop paying monthly for something that only works after the damage is already done.

Your money should be protecting your phone. Not funding their business model.